Multi-asset investing in fast-moving times

How investors can achieve diversification with their portfolios

Achieving true diversification today, amid the increasing complexity and velocity of today’s financial markets, requires greater flexibility over asset allocation and access to more asset classes

And while inflation may be flat or not rising as sharply, it is still high.

This all presents many challenges and opportunities for investors, which will be discussed in this report, worth 30 minutes of CPD.

One in five advisers add thematic equities to portfolios

One in five advisers are adding thematic equities to multi-asset portfolios, representing a minority among their peer group, a FT Adviser poll suggests.

Nevertheless, the straw poll also indicated that advisers are almost even on whether or not thematic equities have a role in multi-asset portfolios at all.

More than half of respondents said they already add thematic equities to a multi-asset portfolio (21 per cent), or would consider doing so (36 per cent). Less than half (43 per cent) said they would not.

Thematic investing, as defined by index provider MSCI, is a top-down investment approach that relies on research to explore macroeconomic, geopolitical and technological trends.

“The themes we like for the long term include the digital economy, with the ongoing transition of economic activity into the virtual world, and the dominance of certain increasingly monopolised companies in this area,” says David Jane, a fund manager in Premier Miton’s macro thematic multi asset team.

“Our energy transition theme includes businesses that benefit from the growth of alternatives to fossil fuels in the electricity markets, currently with a focus on nuclear generation,” he adds.

“We also have a long-term emerging consumer theme, which is currently benefiting from the growth of India. And a major recent theme has been the de-globalisation/re-shoring theme, which concentrates on US industrial business and capex beneficiaries.”

The thematic element has many advantages, according to Jane, one of which is adding an extra dimension of return on top of macro drivers. “The themes can be longer term and consistent over time, and to some degree can be independent of the macro ebbs and flows in markets.

“In essence, by exposing the equity portfolio to a range of long-term ongoing trends we can bias the funds to success, in addition to our value added in asset allocation.”

But in the shorter term, investors should be aware that thematic equity strategies can have a return stream which differs significantly from that of a broader market capitalisation-weighted benchmark index, says Raul Leote de Carvalho, deputy head of the quantitative research group at BNP Paribas Asset Management.

“The difference arises from the fact that thematic funds invest only in the few companies exposed to a given theme, thereby introducing not only the risk related to the exposure of their businesses to the theme, which is expected to generate a premium, but also potentially creating systematic portfolio biases resulting from overweighting some sectors, regions and styles.

“When adding thematic investments to multi-asset portfolios, investors should invest in multiple themes, choosing an allocation that diversifies away their systematic biases as much as possible,” Carvalho suggests.

“While this can be attempted using naive approaches, it is more efficiently done with risk management and portfolio optimisation methods that shuffle the allocation of all assets in the portfolio so that the sector, region and style biases remain unchanged after adding the thematic investments.

“This is required if portfolio returns are to be incremented by the thematic premiums only,” Carvalho warns.

Multi-asset investing in unusual times

Diversifying portfolios has become harder as equities and bonds have become increasingly correlated.

In the decades running up to 2020, the 60/40 approach to portfolio construction, using bonds to diversify equity worked particularly well, as bonds and equities were negatively correlated.

But in 2021 and particularly in 2022, bonds failed to provide the diversification of returns seen in many prior years.

As James Klempster, deputy head of the Liontrust multi-asset team explains, this was fundamentally the result of an exceptional set of macroeconomic headwinds that saw inflation soar to 40-year highs.

Klempster adds: “Since the global financial crisis, the bond risk/reward equation has been distorted by quantitative easing and zero interest rate policy.

“However, this is no longer the case and central banks now have the monetary tools to deal with the next crisis, while balanced portfolios have the downside protection from bonds.”

So while the investment landscape may have improved somewhat, is it plain sailing for multi-asset investors, and how easy is it to diversify a portfolio?

Liquidity issues

Darius McDermott, managing director at Chelsea Financial Services, says: “Very few assets have been able to escape the liquidity drain of higher yields and quantitative tightening.

“This is the deflating of the massive asset bubble that was formed in the years prior from quantitative easing and low interest rates. In this environment, it has been very hard to diversify. However, we still think it is important to do it.”

Klempster says diversification will require greater flexibility over asset allocation and access to more asset classes.

He adds: “The increasing complexity and velocity of today’s financial markets present many challenges and opportunities for investors. Over the next decade, the drivers of successful investing will be different from those of the past 10 years.”

Since the global financial crisis, the bond risk/reward equation has been distorted by quantitative easing and zero interest rate policy

David Jane, a fund manager in Premer Miton's macro thematic multi-ssset team, says: "The 60/40 approach to [portfolio] construction, using bonds to diversify equity worked particularly well for the decades up to

2020.

"This was because of ultra-low inflation and rates. This era has now passed and we are back to a more normal environment where equities and bonds positively correlate.

"Hence we need to use bonds primarily for low volatility and income, particularly at the short end. In the long term, diversification will come from a blend of equity, short-dated bonds and real assets such as property and commodities."

The economy

In the UK and Europe, economic leading indicators are weak and weakening.

Lindsay James, investment strategist at Quilter Investors, points to market data which shows that in the UK the effective interest rate on outstanding mortgages is at 3.14 per cent, while the average quoted rate for new or refinanced mortgages sits at around 5.5 per cent.

With around 30 per cent of mortgages due to be refinanced over the next two years, homeowners are still likely to face a painful upward adjustment of their payments, acting as an ongoing headwind for the domestic economy.

And while Europeans enjoy much longer-term fixed-rate mortgages, as they do in the US, the European economy is nevertheless evidently struggling, particularly due to the global downturn in manufacturing that shows little sign of abating.

This, James says, explains why the International Monetary Fund projects GDP growth in the UK to be just 0.6 per cent in 2024, with clear risks to the downside.

Not all bad news

For investors this is not all bad news. James says: “Should the economy be even weaker than is already anticipated, it could bring inflation to heel more quickly and allow more significant cuts to interest rates.

“We have found that, historically, when the Bank of England has cut interest rates following the end of a period of interest rate rises, returns have been particularly strong in the year after.

“Following the first cut in rates in 1990s, the MSCI UK Index returned 46.1 per cent over the next 12 months. In contrast, the US economy remains on a higher path and there is no certainty that earnings will in fact be weak in 2024. The jobs market continues to be strong while real disposable incomes have been growing.”

Protecting against inflation

It is true that inflation is currently flat in the UK, but it is still too high.

To protect against inflation in a multi-asset portfolio, energy assets and commodities can help, according to investment managers.

McDermott says: “The best protection against inflation has historically been energy stocks, so it might be worth having a little exposure to these. Treasury inflation-protected securities (Tips) or Linkers are another good option now.

“They were a terrible option last year when real yields were negative and they massively underperformed as a result. However, now you can lock into safe real yields of 2.5 per cent.

“This is a good allocation as part of a balanced portfolio in our view. Gold is another traditional hedge against inflation.”

Jane says a balance of short-dated bonds for income and stability and a focus of value, such as resources and energy in equity, with some commodity exposure should perform well.

Jane adds: “In an inflation environment there tends to be greater volatility, bonds tend to underperform real assets and commodities do well. Within equity, value and asset-based businesses do better than growth companies.

Should the economy be even weaker than is already anticipated, it could bring inflation to heel more quickly and allow more significant cuts to interest rates

“We wouldn’t dismiss those companies with pricing power such as the US large-cap tech monopolies.”

According to Liontrust's Klempster, if investors are concerned about whether their returns can exceed price rises then the current rates of inflation and interest rates mean they must look to non-cash assets if they are to have a prospect of doing so.

Additionally, the shortfall of cash versus inflation on current rates will only be exacerbated the longer that investments are parked in savings accounts that pay negative rates versus inflation.

Klempster adds: “Cash plays a role in balancing the risks in diversified portfolios, but the world offers a much wider choice of investment assets with the potential to enhance long-term returns.

“The evidence points to equities being the best way to beat inflation over the long term, which lies at the heart of our own portfolio construction. The key issue for investors is to balance the asset mix to ensure it matches their own risk profiles.”

Protecting portfolios

At Quilter Investors, James says that while they have a range of tools to consider, they can only play a part, and do not fully offset the impact of inflation over a short time period.

She adds: “What is more reassuring is that over longer time periods, such as five years, data shows that large-cap stocks can do a much better job of beating inflation than cash. So the first way to protect against inflation is to remain invested.”

At the portfolio level, James says the first defence would be at the asset class level in considering the optimal allocation to government bonds in particular, which typically bear the brunt of rising inflation and higher base rates.

She adds: “We have been underweight this part of the portfolio for some time across our product range but are finding more attractive opportunities in this area given the level of yields now on offer.

“While bond yields are higher, giving more potential for capital appreciation in a growth shock, this is contingent on inflation continuing to fall, otherwise rate cuts may not be forthcoming, so searching more broadly for portfolio diversification is important.”

The best protection against inflation has historically been energy stocks so it might be worth having a little exposure to these.

Within the equity space, James says quality stocks are best placed to weather the storm of inflation, as these businesses can typically pass on higher input costs to customers without suffering an ensuing hit to demand.

She adds: "They may own a ‘must-have’ product or have a degree of market dominance that is hard to dent; companies like Microsoft and Alphabet spring to mind here.

"Also in the equity space, listed infrastructure assets can also see a degree of inflation protection; on one hand, higher bond yields reduce the value of their future cash flows, but those cashflows typically have a degree of inflation-linkage in their nature.

“Finally, alternatives provide a range of assets that help to protect against inflation. Commodities might fit in here and typically act as a good diversifier in a high-inflation environment. There are also hedge fund strategies such as global market funds and market neutral funds that have done well against the inflationary backdrop.”

Corporate pressure

When it comes to corporate bonds, investors have been used to very low defaults for a long time as companies have been able to muddle through.

But the impact on companies as they refinance to higher coupon rates means more companies will become distressed and go bankrupt as they approach refinancing, McDermott says.

Higher interest costs are likely to put the brakes on expansion plans as companies will have to pay more in interest and will be wary of taking on more debt.

But the picture will not be the same for all companies.

Premier Miton’s Jane says that for the vast majority of large-cap companies, debt burdens are not an issue. Indeed higher rates have come with higher inflation and hence higher revenue.

He adds: “For smaller companies these typically finance with bank debt at variable interest rates, so here the pain has already been felt. The problems will arise as more risky companies, such as leverage buyouts, have to refinance in the bond markets.

“These will really hit it in the coming years and may prove painful or even terminal for some. We avoid the highest risk parts of the bond market, particularly leveraged finance.”

Quilter’s James notes that investors have been needing to delve into balance sheets and ensure they fully understand the incoming impact to interest costs.

She adds: “The implications of debt refinancing are going to differ sharply depending on balance sheet strength and the underlying maturity of the company’s debt arrangements.”

Typically, small caps have a far steeper refinancing ‘wall’ as bond maturities have been shorter, while large caps have been able to use the long period of cheap money to lock in low rates for some years ahead.

For long-term investors, there is a need to embrace volatility

Furthermore, big tech can go one better given the massive cash piles that companies such as Apple, Alphabet, and Microsoft enjoy, notes James.

“Perhaps partly explaining why the mega-cap equities, which are typically growth stocks, have performed so well in 2023 despite the backdrop of rising bond yields,” James adds.

“This has already been a factor in performance with MSCI World Small Cap index delivering -3.84 per cent so far this year (to October 31) while MSCI World Large Cap index has grown 9.22 per cent, arguably suggesting that a large part of this refinancing risk is perhaps already reflected in share prices.”

Arguably, we are through the worst of inflation, and it is anticipated that inflation will continue to fall, as the rolling base effects from Covid shutdowns and Russia’s invasion of Ukraine work their way through the system.

Klempster says this should allow central banks to tread carefully and be less aggressive on the hiking front, but adds that there also remains a risk of policy surprises or unintended consequences, neither of which are supportive for markets.

He says: “For long-term investors, there is a need to embrace volatility and it is likely that over the coming year there will be periods of below average trend returns, similar to those seen in 2022.

“However, with the repricing of bonds and equities it may be a good time to look again to balanced portfolio investing. Claims of the death of the 60/40 approach may be premature.”

Meanwhile, McDermott argues the 60/40 approach is "overly simplistic and misses out on great return and diversification opportunities".

He adds: "We love the alternative investment trust market. Despite its recent challenges we still very much believe in it. We love being able to put different assets in the portfolio at high yields with little correlation to the economic cycle.

"While capital values may move around, we tend to focus on the sustainability of income and we need something more than just traditional equities and bonds to achieve that, and Covid proved this when many equities cut their dividends.

"Investors also need to be wary of liquidity mismatches when accessing more esoteric or less liquid assets."

Combining strategic and dynamic asset allocation to deliver better outcomes for your clients

How can you ensure the risk and return balance of a client’s portfolio remains right for them, while providing a smoother investment journey? The answer maybe to combine a dynamic approach to asset allocation, which addresses cyclical and event-driven changes in market risks and opportunities, with a solid underlying strategic asset allocation framework.

The long-term risk and return characteristics of asset classes, while not set in stone, change very little over time.

This is extremely helpful when you are designing an investment strategy to meet a client’s long-term investment goals.

It means you can reliably construct a portfolio framework that matches the risk and return characteristics that your client is looking for.

Yet investment markets move constantly due to external events, cyclical changes in the economic environment and shifting investor sentiment.

This means there will inevitably be times when individual asset classes deliver returns towards the negative extreme of what can normally be expected.

There will also be some moments when the way that asset classes behave in relation to one another does not conform to what would be expected in normal conditions.

We saw this in 2022 when the US Federal Reserve started raising interest rates to fight inflation and the prices of stocks and bonds fell simultaneously.

This has significant implications for the experience a client can have with their portfolio.

If the asset allocation of the portfolio remains static for example, there can occasionally be times when short-term returns can be significantly worse than they may be used to experiencing, which, for some, may prompt second thoughts about sticking with the investment strategy that they signed up for.

Helping your clients stay invested and reach their investment goals

How can you ensure the risk and return balance of a client’s portfolio remains right for them while providing a smoother investment journey and the prospect of a better outcome?

The answer is to combine a dynamic approach to asset allocation, that addresses cyclical and event-driven changes in market risks and opportunities, with a solid underlying strategic asset allocation framework.

This is the approach that the Schroder Global multi-asset portfolios take.

Our investment philosophy focuses on how the market values different assets compared to where we would expect them to be, given our outlook on the stage of the economic cycle.

For example, in the expansion stage of the economic cycle, equities tend to outperform bonds, while in the slowdown phase bonds tend to outperform equities.

To deliver the best outcomes for your clients, it is vitally important to get both the strategic and the dynamic elements of the asset allocation equation right.

To help us with this, we have a team of more than 130 multi-asset specialists based in the UK, US, Europe and Asia-Pacific region, looking at markets from every angle.

Step 1: strategic asset allocation

The strategic asset allocation (SAA) of a portfolio is the main factor that will drive returns over the medium to longer term and should closely reflect both what a client is hoping to achieve and their attitude to risk.

To get this first step in portfolio construction right, we use the long-term capital market assumptions from our in-house economics group, which include assumptions on the level of risk of each asset class and the relationships between them.

It also includes a long-term expected return based on factors that drive economic growth such as increasing population size and improving productivity.

From this, we build a series of graded strategic allocations to reflect the needs of different clients from the most adventurous to the most cautious.

As the long-term return potential, risk profile and relationships between asset classes can change gradually over time, we formally review the strategic allocation framework for portfolios on an annual basis.

SAA evolution in practice

During our SAA review in 2022, we removed a strategic allocation to UK gilts within our portfolios and increased the allocation to global government bonds.

As we have gradually reduced the allocation to UK equities within our portfolio SAAs it made less sense to hold UK bonds, specifically as a hedge for that exposure.

Diversifying exposure across a global opportunity set should help to reduce the overall risk of portfolios by providing better protection against unexpected events that may negatively affect a specific country or region.

Step 2: dynamic asset allocation

To get the dynamic asset allocation (DAA) of our portfolios right, we use a disciplined 'risk premium' investment approach, which decomposes asset classes into their underlying drivers of risk.

We do this because simply allocating across multiple asset classes will not always achieve true diversification.

There can be times when two assets classes that are normally diversifying are exposed to the same underlying risk. For example, in 2022 the key risk to equities was rising bond yields because of the impact that had on valuations. Therefore equities were exposed to exactly the same risk as bonds (ie rising yields).

Our risk premium approach helps us to understand the true drivers of risk and return and how they interact.

It also enables us to form a positive, negative, or neutral view of the relative attractiveness of asset classes at any point in time, which we derive primarily from in-depth analysis of valuations, cyclical factors and technical factors.

Alongside this, we combine quantitative tools with forward-looking scenario analysis to manage risk. We also use in-house sustainability tools to ensure ESG factors are woven into every aspect of our multi-asset research and portfolio construction.

Our specialist teams meet formally once a month to discuss their asset class views and to determine any changes that would benefit portfolios.

As market conditions can move significantly over the space of a few days, we will also make changes at any time when warranted by major events, while always looking to ensure that portfolios are not exposed to any unwarranted risks.

DAA in practice

One example of DAA that we used in the global multi-asset portfolios range was to add an overweight position in broad commodities (which can include oil, metals, and agricultural products) in 2022.

While some DAA decisions can be shorter term, we held this position for the majority of the year. In a year characterised by slowing global growth and rising inflation, most major asset classes such as equities and bonds fell in value, however commodities recorded positive returns.

This was in part because rising commodity prices were one of the primary causes of inflation, but other global factors also had an impact.

Russia’s invasion of Ukraine and China’s zero-Covid policy together created supply bottlenecks in the global supply chain which pushed up the price of underlying commodities.

Delivering better outcomes for you and your clients

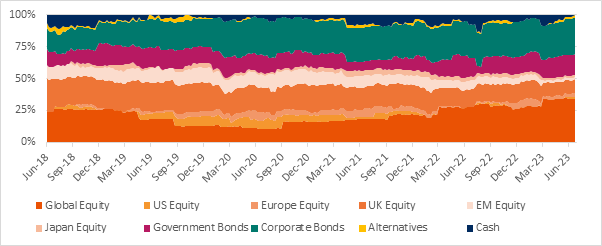

The chart below shows the evolution of the asset allocation of the Schroder global multi-asset balanced portfolio, one of our five risk-mapped multi-asset funds.

The funds dynamically adjust exposures across a range of asset classes in order to adapt to ever-changing market conditions.

The funds offer you and your clients the best of Schroders’ global expertise, combined with both active dynamic and strategic asset allocation and active stock selection, with an ongoing charge figure of just 0.22 per cent.

Active management in action in the Schroder global multi-asset balanced portfolio

Tara Jameson is a fund manager – multi-asset investments at Schroders

Source: Schroders, as at July 28 2023. Alternatives consists of investments which are not a component of the strategic asset allocation. This can consist of, but is not limited to, investments in commodities, emerging market debt, high yield and Reits.